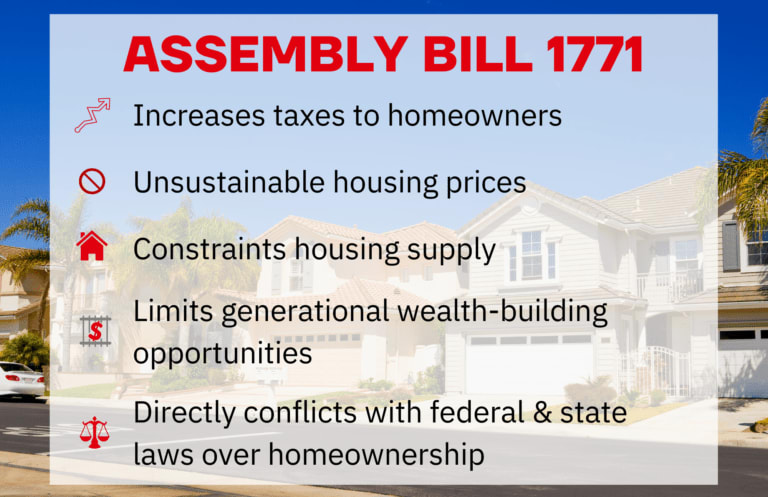

The real estate market in California has been hot and property values have been rising for nearly a decade. This has increased equity for millions and helped to offset staggering taxes in the state. AB 1771 otherwise known as The Housing Speculation Act, is based off of the idea that the increasing price of homes is driven by investor-purchasers of residential properties in California. AB 1771 will reduce our already low inventory and make it harder to find a home.

How Does Ab 1771 Work?

AB 1771 creates a new 25% tax on almost anyone who sells a home in the state of California. If you own a home for 7 years or less and sell, you will pay a 25% tax, which is reduced by 5% each year after year 3. There are exemptions for first-time homebuyers and those in the military, but the potential impact on low inventory may harm buyers more than help.

According to Assemblymember Chris Ward, first-time home buyers are unable to purchase homes due to short-term investors who offer cash payments. By imposing a 25% tax, it diminishes the freedom to move or relocate, housing supply, economic security, and opportunity to grow intergenerational wealth for new homebuyers.

Even Less Inventory

AB 1771 is marketed as a way to help struggling home buyers from competing against flippers and investors who can pay cash. The theory is that flippers and investors pay cash and outbid home buyers causing an increase in home prices. However, AB 1771 will further reduce the already low inventory level of homes for sale. If you thought it was hard to find a home now, wait until sellers are refusing to sell to save money on taxes.

With less inventory, this legislation would result in higher prices due to the reduced supply of homes.

Type Of Real Property Is Covered By The Act

However, the Act would provide an EXEMPTION for the following limited number of real properties:

-

Multiple Unit Affordable Housing

-

Subdivided Properties

-

Designated Open Space

-

Non-Residential Properties

-

Properties Exempt From Transfer Taxes

-

Other Affordable Housing

-

Qualified Taxpayer’s First Primary Residence